In the coming months U.S. Treasury yields/rates could have a dramatic rise.

Most attention is on what action the U.S. – FOMC could take in 2025. The FOMC controls the short-term interest rates, and they are expected to cut rates twice in 2025. They have no control over long – term rates which have been rising for the last several years and could have a large increase in 2025.

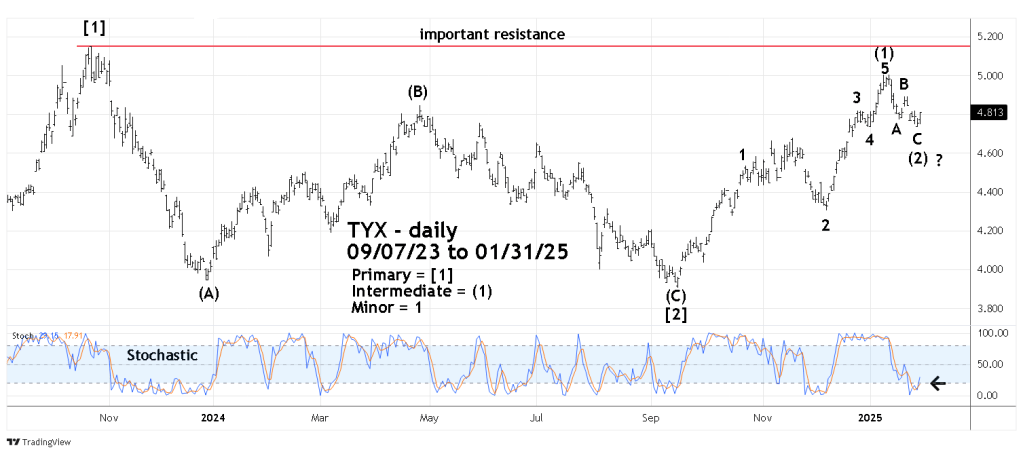

The daily CBOE 30 – Year Treasury Bond Yield (TYX) chart courtesy of Trading View illustrates the Elliott wave action since the major peak made in October 2023.

Since the major bottom in March 2020 TYX has had amazingly clear Elliott wave patterns. From October 2023 to September 2024, TYX decline was an Elliott wave – Single Zigzag correction. The drop was relatively shallow, only retracing about 30% of the upward progress from March 2020 to October 2023. When retracements of the primary trend are shallow it indicates the forces opposed to the primary trend are weak.

The subsequent rally from September 2024 to January 2025 appears to be a completed Elliott – Impulse wave. If so this could be just the first wave of a larger developing bull market.

The decline in January 2025 was an Elliott wave – Single Zigzag and retraced .246 of the upward progress from September 2024 to January 2025. The .246 retracement is very close to the Fibonacci ratio of .236. Additionally, the January decline bottomed at 4.734 almost exactly at the bottom of Minor wave “4” at 4.735.

Daily Stochastics supports the theory that the short-term decline has terminated. Both Stochastic lines reached the oversold zone which begins at 20.00, then had bullish lines cross.

Retracements of .236 usually come when most market participants are aware of the primary trend, which in this case is up. Many times, the movement after a shallow retracement is powerful and sustained.

TYX ended the 01/31/25 session at 4.813, there’s a high probability it could reach the major peak made in October 2023 at 5.152.

If TYX can decisively move above 5.152 it could reach 7.00 or higher sometime in 2025.